Urbanista Dollarization Experiment

Executive Summary

Nudge Lebanon, in collaboration with a local restaurant, implemented a small-scale intervention comprising of a verbal prompt to nudge customers into paying in Lebanese Pounds (LBP) when using electronic payment cards. Staff in one branch were trained to ask customers if they wanted to settle their bills in LBP, purposely omitting USD from the prompt. For exploratory purposes, we also tested the impact of a similar prompt to settle bills in USD. While the prompts resulted in a 3.1 percentage points increase in lira payments at the LBP branch, and a decrease of 1.8 percentage points in lira payments at the USD branch, these results were not statistically significant.

Policy Challenge

The economic instability and political uncertainty in Lebanon in the 80’s and early 90’s, coupled with a severe loss of confidence in the domestic currency, led to the adoption of US Dollars (USD) as a de facto legal tender in lieu of the Lebanese Pound (LBP). At the peak of the economic crisis, the dollarization rate reached a record high of 87% in the third quarter of 1992, before gradually dropping to 61% in 1994 following the issuance of large denomination banknotes by Banque Du Liban (BDL)[1].

More recently, BDL has taken new measures to reduce the rate of dollarization. For instance, in the third quarter of 2018, BDL issued Intermediate Circular No 503 instructing commercial banks to cap their LBP-denominated loans at 25% of the total deposits in domestic currency – a decision that was designed to create an incentive for banks to increase their LBP deposits base[i].

Moreover, in January 2019, BDL issued the Intermediate Circular No 514 instructing all non-banking institutions executing electronic transfers to pay the value of incoming cross-border electronic transfers in LBP[ii].

In addition to BDL’s efforts, several commercial banks have launched campaigns to promote the use of the Lebanese Lira, e.g., Bank Audi[iii], SGBL[iv], and Bankmed[v].

To complement these efforts, Nudge Lebanon, in collaboration with a local restaurant, implemented a small-scale intervention comprising of a verbal prompt to nudge customers into paying in LBP when using electronic payment cards to settle their bills. For exploratory purposes, we also assessed the impact of a similar prompt on bill settlements in USD.

Intervention Design

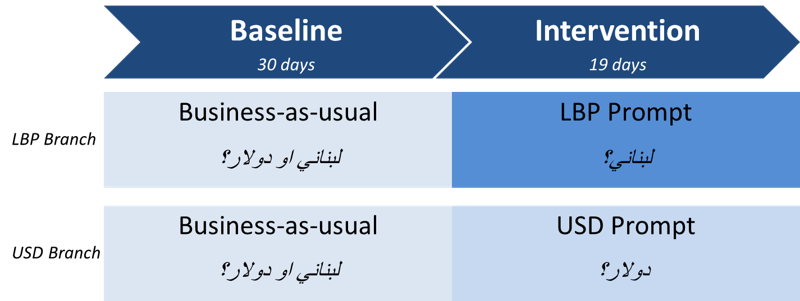

The experiment was implemented in two branches of a local restaurant, for a period of 49 days. The first 30 days involved the “business-as-usual” approach where customers were asked whether they would be paying in USD or LBP upon reaching the POS. During the remaining 19 days, each branch received their own prompt:

- LBP Prompt: Staff in this branch were trained to ask diners if they wanted to settle their bills in LBP, purposely omitting USD from the prompt. Diners were able to settle their bills in USD if they wished to do so; and

- USD Prompt: Staff in this branch were trained to ask diners if they wanted to settle their bill in USD, purposely omitting LBP from the prompt. Diners were able to settle their bills in LBP if they wished to do so.

Figure 1 – Experiment Design

Data was collected for a period of 19 days across the two participating branches, where staff in the LBP prompt branch asked only if customers will be paying in LBP, while staff in the USD prompt branch asked only if customers will be paying in USD.

Data on the number of bills settled using electronic cards for each currency, LBP or USD, were collected from all three branches:

Table 1 – Number of bills settled in each branch

Results

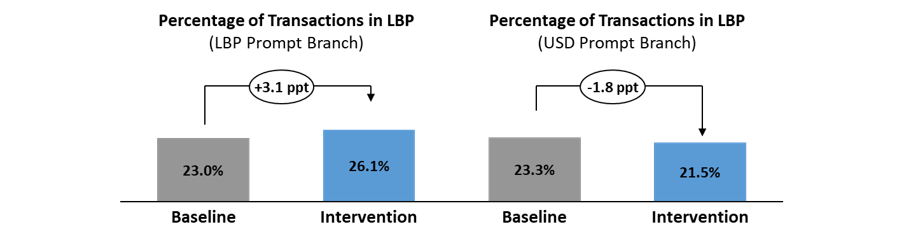

Assessing the proportion of payments made in LBP at the branch that received the LBP prompt revealed an increase of 3.1 percentage points in the proportion of bills settled in LBP during the intervention period (26.1%) compared to baseline (23.0%). However, this different was not statistically significant (p-value = 0.2904; n = 49). Contrarily, the branch that received the USD prompt experienced the opposite effect, where the proportion of bills settled in the local currency decreased by 1.8 percentage points from the baseline period (23.3%) to the intervention period (21.5%). Likewise, this difference was not statistically significant (p-value = 0.6514; n = 49).[vi]

Lastly, assessing the differences in the proportion of local currency settlements between the two branches in the intervention period also yields statistically insignificant results (p-value = 0.1937; n = 38).

Conclusion

While the observed differences between the baseline and intervention period were in line with our expectations (i.e. higher lira payments in the LBP branch, and vice versa for the USD branch), these results were not substantiated as inferential tests do not detect statistically significant differences. This may be due to the small sample size observed which may have reduced statistical power. Alternatively, it could be that the observed differences were due to unobserved time-varying factors which may have influenced the decision to pay in LBP or USD.

Therefore, future replications should consider using a larger sample and an identification strategy that isolates the effect of time-varying variables that may potentially be influencing decisions to settle bills in either USD or LBP (e.g., using randomized controlled trials). It would also be interesting to test an intervention that combines an LBP prompt with messages highlighting the role that citizens can play in supporting the national currency (i.e., inducing national pride).

Endnotes

[1] The issuance of large denominations banknotes by BDL in 1994, was considered a significant step in promoting the adoption of the national currency as part of the de-dollarization process led by the central bank.

[i] Refer to: http://www.businessnews.com.lb/cms/Story/StoryDetails/6892/Inbound-E-money-transfers-must-be-paid-in-lira-only

[ii] Basic Circular No 69 addressed to Banks, and also to Financial Institutions and Institutions Engaged in Electronic Financial and Banking Operations; BDL Intermediate Circular No 514

[iii] “خلّي الليرة ترجع تحكي” : A Campaign Designed to Launch Bank Audi’s “Loubnani” Card. https://www.bankaudi.com.lb/english/press-releases/khalli-el-lira-terja3-te7ke-a-campaign-designed-to-launch-bank-audis-loubnani-card

[iv] SGBL Website, http://www.sgbl.com.lb/sgbl_en/nos-communications/Pages/Campagnes-publicitaires.aspx

[v] Bankmed Youtube Channel. https://www.youtube.com/watch?v=E8oVq6zsMFw

[vi] Given the relatively small sample within each group, it may be that ratio of payments made in LBP does not follow a normal distribution. As such, a non-parametric approach was used in the form of a Wilcoxon rank-sum (Mann-Whitney) test to for estimation of the results.